DeFi for FIs

Happy new year everyone!

The first year for Tech Tok was amazing and very busy, with 31 editions of Tech Tok Weekly and 13 long-form articles published! I went into hibernation mode towards the end of the year, focusing my energy on reading, learning, and diving even deeper into the Web3 rabbit hole, and came out with a bit more clarity around the direction I want to take this blog in.

I’ll focus most of my work this year on doing what I enjoy the most: writing long-form articles about Web3. With the amount of time it takes to brainstorm, research, and write with nuanced depth about this incredibly fast-moving industry, I’ll aim to send out an article every fortnight, and will also include my favourite few articles at the bottom of every post.

Today, we’ll jump into one of my favourite Web3 topics: DeFi, and specifically the financial innovations that underlie it. But first, it’s time for memes!

DeFi for FIs

Unicorns, Sushi, and Financial Innovations

As the total crypto market cap almost quadrupled in value to touch $3 trillion in 2021, the headlines were squarely focused on how the market moved with every tweet from Elon Musk, or on the parabolic returns of Shiba Inu Coin and Dogecoin. As DeFi has taken the crypto and financial world by storm and the DeFi market cap has increased by more than 600%, much of the focus has been on its retail applications, with many financial institutions (FIs) getting put off by the meme-y, jokey nature of the industry. A lot of the hype has been about the ~20% APY that retail investors can make from depositing USD-pegged stablecoins like TerraUSD (UST) into protocols like Anchor, or the token airdrops that can turn early users of a DeFi product into overnight millionaires.

What the hysteria and hype around doggie tokens, joke tokens, and gaming tokens have failed to capture is the true innovation brought about by DeFi: the composability and modularity brought about by the smart contracts powering DeFi protocols. Take Decentralised Exchanges (DEXs) as an example. Abstracting away the fun names (that ostensibly serve their purpose of attracting scorn from established financial institutions), DEXs are a powerful innovation that offer an alternative to the incumbent order book model and allow for newer, less well-established tokens to obtain liquidity and growth. Peeling the onion of other DeFi products yields the same results: catchy, meme-heavy product names underneath which lie financial innovations that, if offered by FIs to their customers, can increase the flexibility and type of products offered, bring about cost efficiencies associated with products like rolling options, and diversify their revenue streams.

There is a bit of a fundamental dichotomy between perceptions of ‘Traditional Finance’ (TradFi) and DeFi: i.e., TradFi and DeFi are on opposing ends of the aisle, and DeFi is everything that TradFi is not – decentralised, non-corporate, accessible to retail investors, and most of all, fun. DeFi has been earmarked as the death of TradFi, but the reality is a lot more nuanced. At its core, DeFi is a set of smart contracts that enable financial innovations which can be used by any party, be it a traditional bank or a day trader working from home. What the drive for adoption of DeFi reflects is consumer preferences for increased transparency, greater access to a wider range of products, higher interest rates in this rock-bottom interest rate environment, a better ability to stitch together their own financial products, and a more social experience. If TradFi firms use DeFi innovations to offer their large number of customers these experiences, it is not necessary for DeFi and TradFi to forever be at loggerheads.

Today, we’ll walk through some DeFi products, their underlying financial innovations, and how FIs can make use of these innovations for their customers. We’ll touch upon:

Enso Finance’s ERC-20 token combinations;

Everlasting Options and how they can transform rolling options;

The Fei-Rari merger and the lessons it offers for automating mergers;

Aave’s interest rate ‘kink’ and what it means for risk management strategies;

Flash loans and the litany of product offerings they bring.

Automated Market Makers (AMMs) and how exchanges can potentially utilise them.

Enso Finance

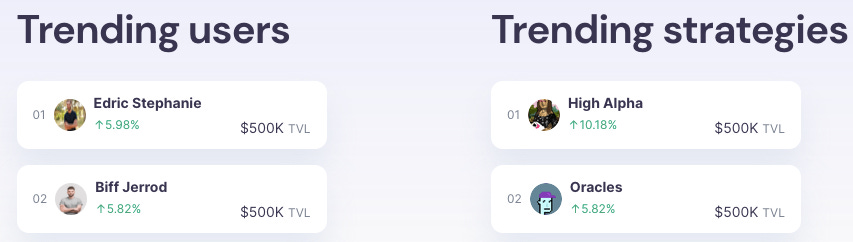

Enso Finance offers the ability to grant users access to any ERC-20 token to combine with any other similar tokens and wrap the lot into another tradable ERC-20 token. Enso allows for any type of token to be bundled together, with no restrictions on the assets that can be included, allowing for yield-bearing tokens or LP tokens that represent liquidity provider positions to be utilised in these strategies. The protocol represents a hallmark of DeFi 2.0, with the inclusion of LP tokens potentially allowing projects to earn additional yield on their protocol-owned liquidity. Enso also offers users flexibility by allowing them to wrap other users’ ERC-20 bundled strategies into their own strategies, showcasing the ‘Lego’-like capability of DeFi strategies. Another key characteristic of the project is its social aspect, with the website prominently showcasing ‘trending users’ and ‘leaderboards’; this enables users to invest in other users’ strategies and could be an indication of how the Web3 social landscape may develop, with a mixture of social plus finance leading the way.

One of the core benefits of tokenisation is its ability to enable liquidity for any type of asset. Assets that are currently extremely illiquid, such as real estate, art, cars, private company interests, etc., can be fractionalised, with ownership in these assets democratised and opened up like never before. All these assets have extremely varied risk profiles; banks and financial institutions can easily combine different types of tokens (representing securities and currently illiquid assets) with different risk profiles into a single token with extremely fine-tuned, bespoke risk profiles. Institutional and retail investors can potentially pick and choose the types and weights of tokens they want to combine into a single bespoke token based on their risk appetites. Investors can also choose to invest in a range of different types of bespoke tokens, all differentiated by the assets that constitute them and their risk profiles.

The social aspect of Enso Finance is also one that FIs can implement. As we have seen through the rise of embedded finance and the ground that banks have lost to challengers, be they corporates offering their customers financial services or neobanks that offer digital-first experiences, customers desire more bespoke products with reduced friction at the point of delivery. Banks have a significant data gap when compared to corporates, who utilise the vast amount of data collected on their platforms to better understand their customers and offer them bespoke products. The social leaderboard-based experience can allow FIs to gather more useful data about their customers, understand their needs more acutely, and reduce the data mismatch these companies have with Web2 platforms. FIs may be able to more accurately judge an individual’s credit history based on the types of investments they have made, feeding into the alternative datasets that have become more prominent to judge credit risk (purchase information, website traffic, order volumes, etc.), and derive more pinpointed customer behavioural insights. SMEs and corporates can also use these bespoke tokens to diversify their treasuries with highly liquid assets of varying risk profiles, earning potentially higher returns on what would previously have been static cash in today’s low interest rate environment.

Everlasting Options

A rolling option is an options contract that grants the buyer a right to purchase an asset at a future date, along with extending the expiration date of that right, for a fee. In today’s world, rolling options is extremely costly since when investors want to roll their positions, they trade with market makers who charge high spreads on every trade. Moreover, rolling positions is risky and involves manual work. Traders may forget to roll, may mis-click, or may execute the trade incorrectly, leaving their positions unhedged, with the lack of automation adding significant friction to the process. The existence of many different options expiration dates also leads to fragmentation of liquidity because market makers will need to spread out their capital to make markets on options expiring every week for the next ‘x’ months. This makes it difficult for other participants to execute large trades or determine fair prices.

Sam Bankman-Fried of FTX fame and Dave White, a research partner at Paradigm Capital, introduced the concept of ‘Everlasting Options’ on the Paradigm blog. Everlasting options build on the concept of the perpetual futures (perps) created by BitMEX in 2016, giving traders futures exposure for as long as necessary without the need to roll. With a perp, those who are long the perp must pay a funding fee to those who are short it, aligning the price of the perp with the price of the underlying asset. This is since if the perp gets more expensive than the underlier, the longs would have to pay high funding fees, incentivising the longs to sell the perp and bringing down its price. In the same vein, everlasting options are the same as a constantly rolling options portfolio and have the same price as that portfolio, with the funding fee mechanism ensuring that price divergence does not last. The mechanism makes sure that the funding payment, at the time of payment, is equivalent to the cost of rolling the portfolio. However, unlike in the case of manual rolling, these new contracts are distributed across multiple expiries, no spreads must be paid, and no execution risk is incurred, significantly reducing the friction of rolling options.

The same principle can be applied by FIs for every tokenised asset, with the automation of the funding fee mechanism leading to a reduction in execution risk and friction, and the creation of more robust hedging markets for all types of assets.

Fei-Rari and Automated Mergers

Fei Protocol and Rari Capital, two of the largest DeFi protocols, completed a merger last month, with Rari transferring its administrative capabilities to TRIBE (Fei’s governance token) and TRIBE assuming control of all governance rights and of Rari’s treasury assets and liabilities. Fei Protocol’s stablecoin FEI aims to be the stablecoin of DeFi, with its USD-pegged token backed by the hallmark of DeFi 2.0 – Protocol-Controlled Value, or PCV. FEI is minted in exchange for whitelisted assets, with $390 million of FEI in circulation collateralised by $1.2 billion of PCV. Rari Capital, on the other hand, allows for the creation of ‘isolated and tailored lending and borrowing pools’ – essentially, a white-labelled version of Compound or Aave.

In the merger process, RGT (Rari’s governance token) would facilitate an exchange into TRIBE at a swap rate of 26.7057 TRIBE for 1 RGT. The exchange rate was defined using a ‘locked box’ in M&A, with a snapshot of the balance sheet of both protocols determined at a specific time (12AM on 16 Nov 2021, when the merger was proposed). The smart contracts governing the merger indicate a lot of flexibility and automation – examples include a ‘TribeRageQuit’ smart contract that allows ‘TRIBE owners at the Snapshot Block to opt out and receive newly-minted $FEI payout in exchange, for 3 days following acceptance of the merger proposal by both communities.’

The merger was ratified on 21 Dec 2021, only a month and 5 days after the initial proposal. While the speed of acceptance reflects the on-chain nature of the governance and assets of both protocols and may not be immediately replicable for almost all ‘real-world’ corporations today, the merger paints a picture of the efficiency, transparency, and speed that can be achieved with primarily blockchain-based organisations. Having some (or all) of a company’s assets and governance on-chain allows for significantly higher transparency in the M&A process, while the flexibility of the smart contracts governing the merger allows for all sorts of terms to be baked into the agreement. Moreover, many mergers do not end up being successful for both parties. A completely automated process may allow for a merger to be scaled back within a specific time period if, for example, both parties agree that sufficient ‘synergies’ (both the holy grail and death knell for a merger) have not been achieved or the integration has been unsuccessful. In the case of Fei-Rari, for example, if a proposal was submitted and accepted to split up both protocols a year from now, the de-merger process of the transfer of governance and assets would be almost instantaneous.

It is important to acknowledge that automated mergers may be possible only for a niche of companies – i.e., for those that are digital-first, internet native, and hold tokenised assets and governance mechanisms that can be transferred instantaneously. While the advent of DAOs may mean that such a world is not too far away, these types of mergers may not be achievable for most companies today.

Aave’s Interest Rate ‘Kink’

When lenders deposit tokens into Aave to earn interest on their deposits, the interest earned is determined based on the supply and demand for that asset and is calibrated to manage liquidity risk and optimise utilisation of the funds deposited. Users are incentivised to support liquidity – when capital is available, interest rates are low to encourage loans, and when capital is scarce, interest rates are high to encourage loan repayments and additional deposits. As explained in this brilliant paper by ING, the borrow interest rate of an asset in Aave derives from the utilisation rate of that asset (the percentage of reserves that have been borrowed from a pool of reserves). The higher the utilisation rate, the higher the interest rate is.

Aave manages the liquidity risk of asset reserves by setting an optimal utilisation rate for each asset, beyond which the variable interest rate for the asset sharply increases. The optimal utilisation rate changes depending on Aave’s risk assessment for a particular asset.

An excerpt from the ING paper illustrates how the kinked interest rate works:

“If Aave set 80% as the optimal utilisation rate for an asset, it means if less than or equal to 80% of a pools reserves are being utilised (borrowed), there will be no kink in the interest rate and the interest rate slope will climb slowly as assets are being utilised. After more than 80% of liquidity is being borrowed from a pool of reserves, a kink ensues and the interest rate slope climbs rapidly to deter borrowers from taking any more liquidity out and encourage paying back their loans. This brings the utilisation rate of the pool back down lower towards the optimal utilisation rate of 80%.”

Financial institutions can utilise a similar kinked interest rate strategy by separating lending pools by the level of risk per pool, allowing for a more pinpointed risk management strategy for decentralised loans. In a world in which corporates or institutions can diversify their treasuries with a range of tokenised assets of varying risk profiles, they could deposit some of those assets into liquidity pools managed by a financial institution. The FI could then lend out those assets and identify a utilisation rate based on the perceived risk of the asset. If, for example, a utilisation rate of 60% is identified for an asset, then the interest rate kink would disincentivise the utilisation rate from crossing too far beyond that threshold. In such a case, the FI earmark 5% of the funds for investment into higher yield-generating assets, potentially passing on the rewards earned to the liquidity providers, paid out either in the underlying token itself or in stablecoins.

Flash Loans

Flash loans are a uniquely blockchain-based product that allow for unsecured (collateral-less) loans. The borrower must pay back the loan before the transaction ends, otherwise the smart contract reverses the transaction. The smart contract for the loan must be fulfilled in the same transaction that it is lent out, with the borrower calling on other smart contracts to perform instant trades with the loaned capital before the transaction ends. Flash loans have several use cases, all of which can be utilised by FIs:

Arbitrage: Traders look for price discrepancies across exchanges for the same asset and utilise flash loans to exploit the price difference without needing to put up any collateral. Banks and hedge funds can use arbitrage bots to find the same types of opportunities being exploited by crypto traders on price differences between DEXs and Centralised Exchanges (CEXs). The opportunity to exploit immaturity in crypto markets is high; Wall Street traders are using ‘old-school finance tricks’ in the crypto market, using complex fast-money trades to exploit price differences across the various protocols and exchanges. The ‘fun’ that used to be had by traders in the immature commodity markets 30 years ago has been replaced by the lucrative trades available in today’s equally immature crypto markets.

Collateral Swaps: Quickly swapping the collateral backing the user’s loan for another type of collateral. Today’s collateral swap market is opaque and using tokens and flash loans to swap collateral on marketplaces can potentially increase the transparency, speed, and security of conducting a swap. Banks could list the types of collateral they want to swap and receive and be matched with another bank with a similar profile, with the swaps being conducted instantaneously using flash loans.

Loan Refinancing: If, for example, a user has borrowed $30 of DAI (MakerDAO’s stablecoin) by locking in $100 of ETH, and a better interest rate is available on another protocol, the user can refinance their loan by using flash loans. Instead of repurchasing 30 DAI to pay back the loan, the user can use a flash loan to borrow 30 DAI, pay the loan back, deposit the $70 worth of ETH into the other protocol, and then use a DEX to swap the remaining ETH into DAI to pay back the flash loan. In a truly tokenised world with all types of real-world assets and interest providers available on the market, banks could refinance loans instantaneously for all types of assets, improving margins and capital efficiency.

Flash Minting: Allow instantaneous minting of an arbitrary amount of an asset, with the newly minted assets existing only during one transaction, being burned at the end of the transaction cycle. Flash minting can be used by FIs for cross-border payments and for token swaps between any two tokenised assets, essentially replacing the need for tokens like Ripple (XRP). For example, if £1,000 is being exchanged for $1,350, in the XRP model, £1,000 would be exchanged for the equivalent amount of XRP in the UK, the XRP would be sent to a digital wallet in the US and converted into $1,350. In a flash minting model, a transaction could be constructed wherein the newly created asset would only exist during that specific cross-border transaction and would be burned when the recipient receives the dollars. This would eliminate the need to create a ‘conversion asset’ like XRP and enable token swaps between a much wider variety of assets, improving liquidity in crypto markets.

Automated Market Makers (AMMs)

AMMs are the central invention of Decentralised Finance, with the way in which they bring constant, 24x7 liquidity to the DeFi ecosystem. AMMs allow digital assets to be traded in a permissionless manner by using liquidity pools rather than the traditional order-book model, where buyers and sellers all offer up different prices for an asset and users who find the same price acceptable are matched. In AMMs, where many tokens are new and have limited liquidity (i.e., the ease with which one asset can be converted into another without affecting its market price), users (liquidity providers or LPs) are offered incentives (fees) to deposit assets into liquidity pools. The price of the tokens in the pool is determined by a ‘constant product formula’.

The utility of AMMs for exchanges could be in their ability to create deep markets for newer, less liquid tokens. Larger centralised exchanges (CEXs) like the NASDAQ, NYSE, and LSE, for example, can spin off smaller DEXs that are meant primarily for penny stocks, start-ups, and assets which may have lower liquidity. In a tokenised world, there will be a multitude of assets of all types that are not offered on traditional exchanges. Many of these assets may not have sufficient trading liquidity and their markets may be immature. The entities offering these assets (for example, the owner of a piece of art who has decided to tokenise and fractionalise that art) could offer incentives to LPs via liquidity pools to provide liquidity for the tokens representing that piece of art. An AMM model could also be applied for specific securities listed on CEXs that do not have sufficient liquidity and could reduce the probability of wash trading, front running, and price manipulation for smaller securities.

The Path Forward

The world of DeFi opens up innumerable avenues for FIs to broaden their revenue streams and increase efficiencies across the board. All they need to do is take a tiny peek under the meme-ridden hood to discover an entirely new world of unicorns, cows, toucans, and the powerful financial innovations that accompany them.

The best articles I’ve read over the last ~2 months:

To join this journey into the worlds of tech, business, and Web3, subscribe below!

Disclaimer

This is a personal blog. Any views or opinions represented in this blog are personal and belong solely to the article authors and do not represent those of people, institutions or organizations that those authors may or may not be associated with in professional or personal capacity, unless explicitly stated. All content provided on this blog is for informational purposes only. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

👇🏽 please hit the ♥️ button below if you enjoyed this post.