On Sanctions, Crypto, and the Weakness of Dollars

On Sanctions, Crypto, and the Weakness of Dollars

A Paradigm Shift in the Global Financial System

Welcome to a cheery Tuesday morning, where we’ll try to offset the gloom from discussing the structural imbalances in the global financial system with memes.

On Sanctions, Crypto, and the Weakness of Dollars

A Paradigm Shift in the Global Financial System

Russia’s invasion of Ukraine is momentous for a number of reasons. For one, it has brought war ‘back’ to Europe in the form of a megalomaniacal strongman aiming to cement his place in the history books. Once the fog of war has dissipated, though, what will likely have a lasting impact is the West’s response to Russian aggression and the slew of financial sanctions that have crippled the 11th-largest economy in the world. Combined with the growing maturity of cryptocurrencies, the impact of sanctions has thrust the importance of decentralised, censorship-resistant money and settlement media into the public domain. The use of sanctions is linked to another global, long-term development: the weakening role of the dollar in the global financial system, the movement away from the petrodollar system, and the potential use of cryptocurrencies (such as Bitcoin, but not necessarily so) as ‘hard monies’ (i.e., those made up of or directly backed by a valuable commodity like gold or silver).

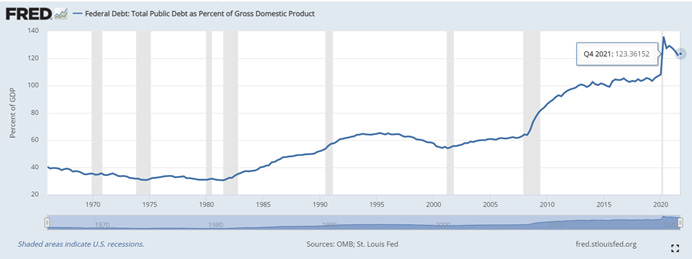

Since the Bretton Woods Agreement in 1944, the US dollar has unequivocally been the world’s reserve currency – a currency that is accepted around the world for transactions and savings. The country that prints the world’s reserve currency is usually the hegemon. It is in a very powerful position since its transactions are paid in its currency and people want to save in it, which enables the country to borrow more at lower rates than other countries since lenders want to lend in the reserve currency. However, having a reserve currency is a poisoned chalice; all past reserve currencies have stopped fulfilling this role, and the end of the use of a currency as the world’s primary currency usually signifies the end of that country’s hegemony. Today, as explored by Ray Dalio in his book Principles for Dealing with the Changing World Order, the US dollar is following right in the steps of the world’s previous reserve currencies (namely, the Dutch guilder and British sterling). It is towards the end of its long-term debt cycle, where it is printing too much money in order to borrow excessively (its debt-to-GDP ratio is at 123.36%, at one point in 2020 having more than doubled since 2008) and sustain the petrodollar system.

When a currency is excessively printed in relation to the demand for it, and value accrues to financial assets rather than to ‘real’ economic activity, it begins to lose its value. At these times, debtholders will want to exchange the debt they are holding for other, more ‘tangible’ stores of wealth.

The decline in a reserve currency’s status happens gradually over time but is bookmarked by notable events. With the US dollar, it seems as if the financial sanctions imposed by the West on Russia, specifically the freezing of $300 billion worth of sovereign international reserves held in the form of securities and in banks to bolster the rouble, seem to have alerted countries to how precarious their financial sovereignty actually is. The morality or necessity of the use of the sanctions is not in question; however, the effect it seems to have had is akin to that of letting the genie out of the bottle. Countries have recognised the need to completely control their financial destinies, which could hint at a slow but steady decoupling from today’s dollar-denominated economic system.

All of these factors, when coupled with the growing primacy of cryptocurrencies, have thrust crypto right into the middle of the conversation. From being used as a tool to donate ~$100 million to the Ukrainian cause on one side to being ferociously debated as a means of evading sanctions, what role crypto will come to occupy in the financial system is becoming top of mind for a whole host of stakeholders. One aspect that is particularly intriguing is the way in which crypto could potentially be used to design a more sound, durable form of ‘hard’ money. Bitcoin is the asset most frequently mentioned in this context as the proto censorship-resistant money, but there are benefits and drawbacks to its use as hard money.

Today, we will:

Explore the role of reserve currencies in the global economic system, how these have operated throughout history, and how the power of reserve currencies inevitably reduces over a period of time;

Walk through where the US, as the hegemon of our time, is in its long-term debt cycle and what impacts the Federal Reserve’s actions post-2008, especially during the COVID crisis (i.e., printing gobs of cash as stimulus) may have on the role of the dollar in the global economy;

Discuss the financial nuclear bomb that has been detonated on Russia over the last month, and the possible impact it could have on the global role of the US dollar;

Delve into what the characteristics of sound, durable money are;

Talk about the emerging role of cryptocurrencies in the financial ecosystem and analyse the position that Bitcoin could occupy going forward as a reserve asset or hard money.

The Reserve Currency and Long-Term Debt Cycles 🔁

Throughout history, one of the greatest benefits brought by a reserve currency has been the buying power and geopolitical power it imparts. At the start of a reserve currency’s rise, it is linked to hard money, commonly gold, and the number of claims on the hard money (i.e., amount of currency circulating) is equal to the amount of hard money in the bank. Over time, however, due to the power of debt, the amount of currency grows to exceed the amount of hard money held. For a reserve currency, this usually occurs because the issuing country borrows more at lower rates since it is the world’s leading trading power.

The excessive borrowing (above the amount of hard money backing the currency) is unsustainable. After a certain point, the conversion from debt to hard money becomes impossible when the number of claims held to buy goods and services increases faster than the available goods and services. There is an inevitable economic decline, which leads to a bank run where currency holders attempt to cash out of the currency and get their hands on the underlying hard money. The bank has two choices:

The tougher option, which is to allow the flow of money out of the debt asset (which increases interest rates and leads to greater economic troubles);

The easier option of de-pegging from the hard money and moving to a fiat currency system where more money is printed by issuing and buying bonds to prevent interest rates from rising.

While central banks may initially choose to go with the tougher option and increase short-term rates, they usually increase the money supply when the economic pain is too high. This devalues the money, increases inflation, and leads to the same debt cycle of excessive printing and devaluation repeating.

A breaking point is reached when the newly printed money does not go into activities that increase demand in the real economy, but rather flow into financial assets, inflation-hedge assets, or other currencies. According to the BIS, an ‘exogenous increase in financial sector growth can reduce total factor productivity growth’. Moreover, once a country is at a certain level of financial development, Brookings asserts that there is no reason to expect that credit expansion leads to more long term growth. Rapid credit expansions can also lead to a decrease in lending standards, over-exposure of the financial sector, and macroeconomic imbalances. At these times, inflation can also be very high, and when it is higher than wage growth, this disproportionately increases inequality since financial assets are held in much higher proportion by the rich than the poor.

All of the macroeconomic pain reaches a crescendo at the end of the long-term debt cycle, when the overriding perception is that the reserve currency and debt denominated in it are no longer good stores of wealth. Consequently, there is a considerable amount of economic pain that leads to a step change in the composition of money and there can be a painful move away from the devalued, debased reserve currency to some form of hard money or a link to a hard currency that is re-established.

The State of the Dollar-led Reserve Currency System 💵

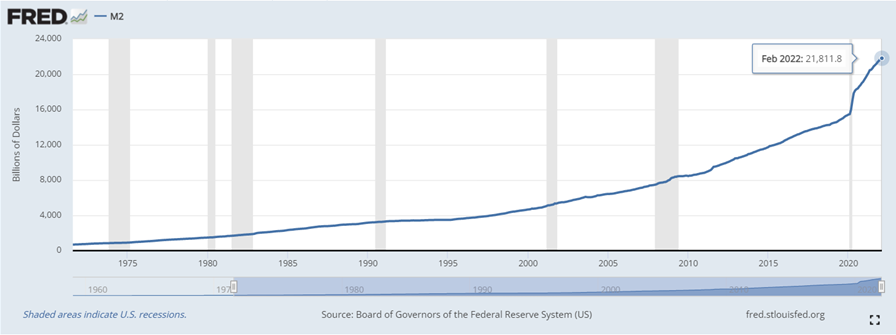

The current long-term debt cycle that is in its latter stages was established in Bretton Woods in 1944, which required currencies to peg to the US dollar, which was in turn pegged to gold. All of the countries in the system pegged their currencies to the dollar and monitored and maintained their pegs by using their currencies to buy and sell dollars. Between 1944 and 1971, the dynamics of the dollar mimicked those of previous reserve currencies. So much money was printed that the US’ gold supply (the hard money backing the dollar) was no longer enough to cover the number of dollars in circulation. After a run on the gold reserves in August 1971, President Nixon took the decision of de-pegging from gold and moved to a fiat currency system where the US was free to print as much money and create as much debt as needed. It has indeed done exactly that, with M2 having increased by 3,081.88% since August 1971, at a CAGR of 61%.

Along with the de-pegging from gold, the 1970s saw another crucial development as well – the creation of the petrodollar system, which further supercharged the printing of dollars and cemented demand for dollars universally. The US made a deal with Saudi Arabia and other OPEC countries to only sell their oil in dollars, regardless of the country buying the oil, in return for military protection and trade deals. Any country in the world that needed to import oil thus needed dollars to do so, ratcheting up demand and cementing the US’ central role in the world economy. Currently, the dollar accounts for 50% of global trade invoices and countries making up 70% of global GDP peg their currencies to the dollar.

With almost every country in the world transacting in dollars, it gives the US carte blanche to impose sanctions and cut countries off from the dollar-based system to devastating effect, as we are currently seeing with Russia. The problem with all the money being printed, however, is that it has made US exports more expensive and imports less expensive, and contributed in some way to the hollowing out of the industrial base of the country. Moreover, the US has expended tremendous resources to ensure military protection of the Middle East, which has added to its structural trade deficits and contributed to over-extending the dollars’ power beyond its fundamentals, which is another sign of the declining power of a reserve currency.

The picture has become even starker over the last couple of years. Public debt as a percentage of GDP has ballooned since 2020, while M2 has increased by ~41% over the last two years alone. The stability of the fiat system is waning and faith in the dollar is reducing. The financial sanctions imposed by the West on Russia and the US’ control on other countries’ financial sovereignty has also become blindingly clear.

Sanctions: The Financial Nuke 💣

As a response to Putin’s aggression, Russian banks have been shut out of the correspondent banking system for dollar transactions and were given a 30-day notice to close their accounts at US correspondent banks. SWIFT disconnected 7 Russian banks from its network, and most devastatingly, the West has frozen $630 billion worth of sovereign international reserves held by Russia. Of this, $400+ billion (>20% of Russia’s GDP) was held in European and other fiat assets, which has left Russia in an extremely precarious position. The affected assets (amounting to ~$300 billion held in securities and in banks) led to the value of the rouble immediately dropping by 50% and in response, the Bank of Russia forced exporters to sell 80% of their FX receipts for roubles.

Using such a ‘shock and awe’ strategy works only once. It has alerted governments and central banks to the fragility of the global economic system for almost every country apart from the US – who has the most to gain from the indefinite maintenance of this system but also the most to lose if it is dismantled. Globally, $13 trillion of FX reserves (14% of global GDP) have been accumulated, with 59% of this held in securities denominated in dollars, 20% in euros, 6% in yen, 5% in sterling, and the rest in other currencies. If the countries that hold the largest amount of these reserves (such as China or Saudi Arabia) get on the wrong side of the US or the West in general, it is conceivable that their financial sovereignty is crippled by sanctions. As a result, the dollar’s role as being a universal store of value is being seriously questioned, and countries are making some moves to divest away from the dollar.

Saudi Arabia, firstly, is in talks with China to price some of its oil sales in renminbi. While this may seem to be trivial on the face of it, the impact could be meaningful. This marks the first significant shift away from the petrodollar system – China buys more than 25% of the oil exported by Saudi Arabia. While 80% of oil sales worldwide are conducted in dollars today, if a large chunk of those are instead priced in other currencies, the supply of dollars in the market would exceed the demand for it, causing monetary inflation and leading to diminishing trust in the value of the dollar as a store of value.

Secondly, another indication of the relative ‘weakness’ of the dollar could be demonstrated by countries either de-pegging their currencies from the dollar or creating bilateral currency trading pairs. In the Saudi Arabian case, economists have said that ‘moving away from dollar-denominated oil sales would diversify the kingdom’s revenue base and could eventually lead it to repeg the riyal to a basket of currencies, similar to Kuwait’s dinar’. India, on the other hand, has attempted to stay neutral in the Russia-Ukraine conflict, and is exploring ways to create a rupee-rouble trading pair to continue trading with Russia.

If all of these developments happen on a wider scale, demand for dollars could decrease across the world. It would also diminish the US’ ability to continue printing the dollar to finance its huge budget deficit, which totals more than $2.5 trillion. In the worst-case scenario, debtholders could flee from the dollar to other stores of value, severely impacting the dollar’s role as a reserve currency.

But what do those other stores of value need to have in order to effectively ‘replace’ the dollar as a global settlement medium?

The Characteristics of Sound, Durable Money 💯

Over the past few weeks, a lot of people have tried to answer the question of what money is. Lyn Alden effectively boiled down the characteristics of what sound money should be:

Divisible: able to be divided down into various sizes to account for different sizes of purchases;

Portable: easy to move across distances;

Durable: easy to save across time;

Fungible: one unit is exactly the same as another unit;

Verifiable: the seller of the goods or services for the money can check that the money is valid;

Scarce: the money supply does not change quickly and devalue existing units;

Utility: the money is intrinsically desirable in some way.

There is a fundamental difference between money and currency. Currency can be defined as the liability of an institution (commercial or central bank), while money is not a liability, but rather is something that has more intrinsic value. As we’ve seen with the gold-backed currency system, money has been used as a reserve asset to back currencies. An important characteristic of money is also its stock-to-flow (S2F) ratio, which measures the scarcity of the money. The ratio compares an asset’s current stock to the rate of new production, with a higher ratio equating to higher scarcity. An asset with a high S2F ratio is expensive to produce and relatively rare, but a lot of it has already been produced and is widely distributed and held. Gold has usually been the flag-bearer for strong, durable money. Its S2F ratio has fluctuated between 50 and 100, indicating its rarity and scarcity, and currently sits at 62, meaning that it will take 62 years to create all of the gold in existence today. The main problem with gold, though, is its divisibility and ability to be used for day-to-day transactions. It is not conceivable that you go to your local supermarket and plop down some gold to the cashier to pay for your groceries. Moreover, physically holding the gold is not feasible for everyone in the world.

Money is also a convention. While it is commonly accepted that gold has intrinsic value, this may not be entirely correct. The use of an asset determines its intrinsic value. While gold has some industrial value, over time, its price has increased disproportionately compared to its actual usage. This may indicate that gold has a lot of extrinsic value and a strong belief system that has formed around it, buoyed by its ornamental value and use throughout history. Moreover, it is not necessary that money have intrinsic utility. If something is a utility, the best use for it is to be consumed or used to create some sort of product. By storing it instead of using it, it is tied up and prevented from being used optimally. Therefore, gold can be seen to have some intrinsic utility, but not a lot.

Over the last decade, another asset with a similar profile to gold has emerged: Bitcoin.

Bitcoin, Crypto, and Hard Money ₿

It is important to analyse how Bitcoin can be used as hard money by assessing it against the characteristics described above. Bitcoin is extremely divisible and is able to be divided into units as small as 0.00000001 BTC; it is available on nearly 600 exchanges, making it very portable; its entirely digital format makes it very durable, ensuring that it does not tarnish over time; it is fungible; the nature of the blockchain makes each Bitcoin transparent, immutable, and fully verifiable; and its S2F ratio of 52.3/54.4, indicates scarcity akin to that of gold. Bitcoin’s utility is the point that is most contentious regarding its classification as hard money.

Bitcoin does not have intrinsic value, although its extrinsic value is definitely on the rise. There has been a lot of debate around whether Bitcoin is actually useful, but there is a strong argument to be made, especially in today’s political climate, that a censorship-resistant and transparent currency like Bitcoin is extremely useful. Firstly, Bitcoin represents true technical innovation. It solved the Byzantine Generals Problem which had been unsolved for decades through the creation of the Proof of Work consensus mechanism, and also was the first to solve the problem of double spend that had been an obstacle to the creation of digital money without a central authority. Secondly, Bitcoin holds a lot of cultural value by virtue of the entire ecosystem of services and trillion-dollar industry it has spawned. To many people, it also represents a vision of a censorship-resistant money that is not controlled by a centralised entity and is representative of a world without the negative externalities imposed by the manner in which big tech companies are run today. Ideas and narratives are powerful, and similar to the belief system around the value of gold, Bitcoin has a strong one. It remains to be seen how this holds up over the future, especially in light of regulations getting more concrete over the world. Lastly, Bitcoin does an even better job than gold in having no intrinsic utility. It only has a monetary premium and no utility, which may make it the soundest form of money since its only use should be as money.

Bitcoin does have drawbacks, though. For one, it probably cannot be used as a currency. Currencies need to be used by people every day. Bitcoin’s transactions per second (TPS) is way too slow at 7 TPS, even with the implementation of the Lightning Network scaling solution. It is not the most efficient way to exchange value but is more suited for acting as a long-term store of value (akin to gold) and a safe haven in times of distress. This is primarily due to its censorship-resistant characteristics, where the supply is fixed, all the rules relating to its monetary policy are coded in and transparent, and it is incredibly difficult to hack. It can also be self-custodied, meaning that it cannot be seized by governments, which is seeming like a more attractive characteristic every day. Bitcoin’s use as a safe haven asset is becoming increasingly apparent, with Russia’s political opposition, Nigerians protesting against police violence, and Russians and Ukrainians alike turning to it recently.

Another potential negative to Bitcoin has been its environmental impact, although this is a point of fierce debate as well. Bitcoin mining consumes 121.36 terawatt hours a year, which is more than Argentina consumes and more than the consumption of Google, Apple, Facebook and Microsoft combined. However, the computers used to mine Bitcoin use a mix of different energy sources; because Bitcoin can be mined anywhere, it can use power sources such as hydro and flared natural gas (excess gas released by the process of oil extraction that would have otherwise gone unused) that are inaccessible for many other applications. Exxon Mobil recently announced that they would use excess natural gas to power Bitcoin mining operations in the US, indicating that mining could get a lot more energy-efficient soon. However, the overriding narrative today is that Bitcoin is bad for the environment. Unless this changes both in practice and perception, Bitcoin will face substantial opposition to its adoption as hard money.

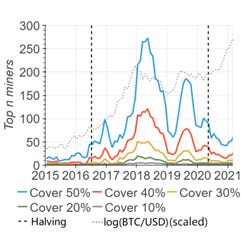

There is also a narrative that only a few wallets control almost half of Bitcoin in circulation, and that mining capacity is highly concentrated. Some of these addresses belong to cold wallets owned by centralised exchanges, institutional trusts that hold BTC on behalf of others, and wrapped BTC that is used on other blockchains. However, individual investors control 8.5 million bitcoins, almost half the bitcoins in circulation by the end of 2020. Mining is also dominated by only a few pools, increasing the risk of centralisation and a 51% attack. In 2021, just over 50 miners were necessary to cover 50% of the market, as shown below.

Unless this large risk is addressed, it will either inhibit adoption or will reflect today’s centralised paradigms, both of which are undesirable outcomes.

Bitcoin’s volatility is also used as a (fair) argument against its use as a currency or hard money. Bitcoin is more volatile than the three major currencies (dollar, euro, and yen). Daily volatility is regularly around 10% and can even reach 30% on some days, which makes the exchange of the asset as a currency unfeasible since the purchase price of a good can highly vary from one day to another. Bitcoin is 3.5x more volatile than gold as well, and even though this can be attributable to the asset being relatively young, it also shows that Bitcoin has a long way to go if it is to be used as a long-term store of value or hard reserve asset.

The ideal form of hard digital currency needs to be a more efficient payment instrument, employ a more energy-efficient consensus mechanism, have more distributed ownership, and be more stable over time while imitating Bitcoin’s characteristics of hard money and developing a strong narrative about itself. This is not an easy proposition, but if it is achieved, it could play a critical role as a reserve asset that can be used ubiquitously for payments.

Closing Thoughts ⌛

The Russian invasion of Ukraine and the subsequent financial sanctions imposed on Russia have opened up Pandora’s Box. The role of the US dollar as the world’s reserve currency and primary settlement medium is being seriously questioned. With the US being in the latter stages of the long-term debt cycle and the ways in which previous reserve currencies have stopped being reserve currencies, combined with some early moves by countries to attempt to diversify away from the dollar, there seems to be a need for a censorship-resistant form of hard digital currency. Bitcoin could end up playing an important role, with its characteristics meeting those of hard money, but its inadequacy as a day-to-day payment instrument means that another form of currency may be necessary. What is abundantly clear, though, is that we are witnessing a paradigm shift that could have a momentous impact on the future of the global financial system and looking to the past and matching it with the trends we’re seeing today may be the best way of predicting how this all pans out.

🔝Reads

To join this journey into the worlds of tech, business, and Web3, subscribe below!

Disclaimer

This is a personal blog. Any views or opinions represented in this blog are personal and belong solely to the article authors and do not represent those of people, institutions or organizations that those authors may or may not be associated with in professional or personal capacity, unless explicitly stated. All content provided on this blog is for informational purposes only. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

👇🏽 please hit the ♥️ button below if you enjoyed this post.