What's Catching My Eye in DeFi

What's Catching My Eye in DeFi

UXD, Dopex & Alkimiya

Welcome to Tech Tok this fine Monday in May. Macron’s been re-elected as President, Netflix has burned subscribers and market cap, and the market is completely risk off amidst worsening macro conditions, war, and shooting inflation. Cheery!

What’s Catching My Eye in DeFi

UXD, Dopex & Alkimiya

DeFi is one of those areas in Web3 that, at the same time, is much vaunted and heavily criticised. After DeFi Summer 2020, where the Total Value Locked (TVL) in DeFi protocols increased by more than 2,800% from $601.65 million to $17.71 billion, DeFi was the poster child of the Web3 ecosystem. While the TVL has continued to rise, reaching an all-time high of $254.72 billion in November 2021 and settling at around $200 billion today, the discourse around DeFi has shifted markedly since. Now, all the attention is on NFTs, the growth of alt-L1s, L2s, bridges, Web3 gaming, the merits and perils of decentralisation, and the marketing buzzword that is the metaverse.

DeFi Summer was characterised by liquidity mining, ridiculously high APRs, and the breakthrough of the AMM into the mainstream. As we’ve seen, though, liquidity mining has proven to be completely unsustainable. Its inflation-based tokenomics has led to the kings of DeFi Summer, such as Compound, being brought to their knees. Compound, for example, distributed more than $300 million in token incentives from June 2020 to September 2021, and earned ~$34 million in protocol revenues over the same period. Even if the liquidity mining program can be chalked off as a marketing expense, Compound has earned only an additional ~$15 million in revenues between October 2021 (when the program ended) and March 2022, at an average of ~$2.5 million per month. Combined with the mercenary nature of capital in DeFi, it seems as if Compound’s liquidity mining program turned out to be a very expensive and ultimately unsuccessful experiment. The underperformance of DeFi is also reflected in its price performance over the last year. Since April 30, 2021, the DeFi Pulse Index (DPI), an index that tracks the performance of the largest DeFi protocols including Uniswap, Aave, Maker, Compound, and Yearn, has dropped in value by ~70%; the price of Ethereum, on the other hand, has increased by 3.5%.

The advent of OlympusDAO marked the emergence of DeFi 2.0, whose protocol-owned liquidity model brought another dimension to the market and tried to solve the problem of providing sustainable liquidity for projects. OHM, and the gazillion forks that followed it, however, failed to truly galvanise DeFi. $OHM purported to be some sort of ‘decentralised reserve currency’ and instead turned out to basically be a hedge fund. Its price reached a peak of $1,334 in October 2021, and has since cratered to $24, a decrease of 98%. OHM’s crash led to many deriding DeFi 2.0 and saying that ‘no true innovation’ has emerged in DeFi for a very long time, with the Curve Wars, the veToken model, and bribing protocols being incremental improvements rather than meaningfully moving the needle in any way.

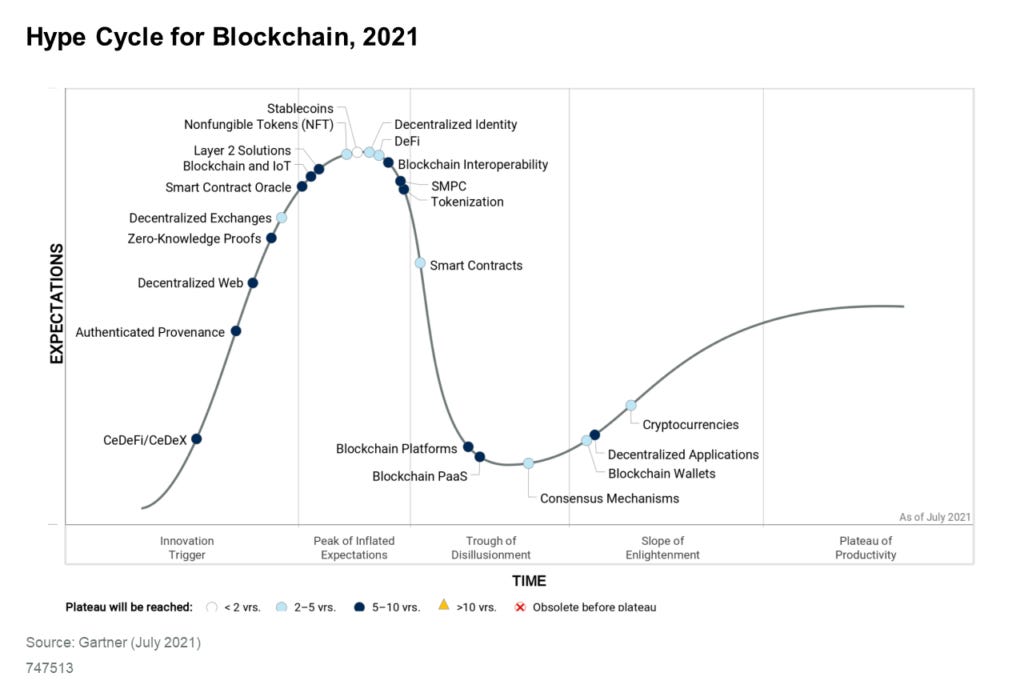

DeFi has been in a bear market for at least the last year, and probably longer. According to Gartner’s Hype Cycle for Blockchain for 2021, DeFi was right at the Peak of Inflated Expectations as of July 2021. By now, it’s slid a long way down the Trough of Disillusionment, indicating that the types of projects that will succeed in DeFi will need to provide tangible benefits for the ecosystem and solve real problems, rather than just being derivatives of innovative products (e.g., DEX #72 on Layer 1 #200).

Contrary to what the naysayers say, some projects are meaningfully innovating in the DeFi space today. Today, we’ll go over three projects that have caught my eye over the last few months and are attempting to expand the realms of what is possible with tokens and blockchains. These projects are:

UXD Protocol, an algorithmic stablecoin;

Dopex, an options and structured products protocol; and

Alkimiya, a ‘consensus capital markets’ protocol.

UXD Protocol 🪙

Stablecoins are one of the most important infrastructural pieces of the Web3 ecosystem, with their stable prices enabling them to be used as a store of value and a medium of exchange within crypto while theoretically having the anonymity and decentralised features of cryptocurrencies. Stablecoins are typically constructed in 3 ways:

Fiat-collateralised, such as USDC or USDT, where each unit of stablecoin issued is purportedly backed by $1 held in a bank account. These stablecoins are centralised and held by one independent party, such as the Circle Foundation or Tether Limited.

Crypto-collateralised, such as MakerDAO’s DAI. Users lock up collateral (such as ETH) in a ‘Collateralised Debt Position’ (CDP) and receive newly issued DAI as debt for their loan. The amount of collateral locked up is higher than the amount of DAI issued, e.g., if the collateralisation ratio is 150%, if $150 of ETH is locked up, then the user receives $100 worth of DAI. The peg to the dollar is maintained via arbitrage incentives on trading venues combined with the demand and supply mechanics when CDPs are opened (stablecoin minted) and closed (stablecoin burned). This model is capital-inefficient, cannot scale well and has the potential to lose its peg if there is a systemic loss of confidence. This happened to DAI in March 2020, when a 30% drop in the price of ETH in one day caused DAI’s value to significantly deviate from its peg. This led to DAI moving from a mostly ETH-collateralised stablecoin to one that is now 60% backed by USDT and USDC and is subject to the same centralisation concerns that fiat-collateralised stablecoins have to reckon with.

Algorithmic, or partially collateralised, such as TerraUSD (UST) or FRAX. These aim to maintain their peg to fiat in a few different ways – Terra, for example, uses a two-token seigniorage model with a volatile asset (LUNA) and the stablecoin (UST), while FRAX uses a fractional-algorithmic model where part of the supply is backed by collateral and part is algorithmic. There has been a lot written and said about how these models work and their drawbacks and benefits, so I won’t explore them today. In general, algorithmic stablecoins are very risky, have shown a tendency to lose their peg (TITAN and USDN are good examples), and no model has definitively succeeded yet. However, creating a sustainable algorithmic stablecoin model is the ultimate goal, given the vast benefits of decentralisation and transparency it provides.

UXD Protocol attempts to solve the algorithmic stablecoin dilemma in a novel way. Launched on Solana, UXD’s algorithmic design is backed by a delta-neutral position on a perpetual derivatives exchange. Let’s break that down.

A position is ‘delta-neutral’ with respect to a particular asset if the value of the position does not depend upon the value of the asset, i.e., it does not matter if the price of the underlying asset moves up or down, the price of the position stays the same.

A perpetual derivative is one where the option never expires, its pre-determined price (strike price) is replaced by the market price (mark price) and does not require settlement. A perp should be worth about the same as its underlying asset, whose price is called the index price. When the index price and mark price diverge, a funding fee mechanism is instituted. When *mark price – index price* is positive, those who are long the asset pay those who are short, and when *mark price – index price* is negative, those who are short the asset pay those who are long. This fee is paid to incentivise users to take the opposite position on the exchange and bring the mark price in line with the index price.

The design to mint UXD works as follows:

A user deposits $1 of BTC to the protocol and, in exchange, receives $1 of UXD;

The BTC is deposited to a perpetual exchange protocol (Mango Markets) as collateral and an opposite short position is taken at the same value of the deposited BTC.

The redemption mechanism flows in reverse:

Users burn UXD with the protocol;

The UXD protocol closes the short position on the perp exchange for the exact dollar amount of UXD burned;

The BTC is then withdrawn to the protocol and returned to the user.

In this model, if the price of BTC falls by 5%, the BTC collateral would lose 5%, but the short position would gain 5%, effectively resulting in a net 0% move of UXD’s collateral.

The UXD Protocol generates revenue in two ways:

Funding Fees: Since UXD Protocol opens up short positions on perp exchanges, it will receive funding fees from users with long positions. Usually, the funding fee is paid from the more popular position (e.g., longs) to the less popular position (e.g., shorts). Since the overriding market sentiment over the last couple of years has been long, the protocol would usually obtain revenue from its positions on the perp exchanges. Since we’re all crypto bulls in the long-term, it can be reasonably assumed that UXD Protocol would be able to count upon positive funding rates as a revenue source in the long-term.

Active Management of the Insurance Fund: In case the funding rate turns negative (as it could during a bear market), the protocol has an insurance fund worth $57 million (funded during the IDO sale of the protocol’s UXP governance token) that it can use to pay funding payments without impacting UXD holders. At its current size, the insurance fund would be able to sustain a year’s worth of -11.4% interest on $500 million of UXD. An idle insurance fund would be capital inefficient; therefore, the protocol is currently exploring asset management strategies for the fund, which will potentially increase revenues for the protocol. However, returns from the fund are uncertain and it may constitute a disproportionate risk to UXD holders to actively manage the fund, especially in choppy market conditions.

The main risk factors / points of instability for UXD’s design are the funding rate and the size of perpetual markets today. These factors are interlinked; the size of perpetual markets today in crypto is extremely small, with crypto options volumes as a percentage of spot at around 2% as of January 2022. This number is 35x in US equity markets, indicating significant room for the market to grow. However, this means that if UXD scales rapidly, the short positions it would open up on perp exchanges would almost certainly drive funding rates negative, putting the onus on UXD to pay longs and deplete its insurance fund. This means that UXD needs to grow steadily in lockstep with crypto options markets, and as the number of perp exchanges increases across L1s and L2s, the proliferation of UXD across these chains will concurrently grow.

UXD’s algorithmic stablecoin design is the closest we have come (so far) to meeting the three tenets of decentralisation, stability, and efficiency that stablecoins all strive to meet. The main knock against the protocol is the initial lack of scalability it will have – however, this is potentially mitigated over the long term as the market matures and options volumes increase.

Dopex 🐃

Options markets are used by almost all market participants in TradFi, including market makers, hedge funds, and retail traders. As an example, 58% of Robinhood’s transaction-based revenues in Q1 2022 were driven by retail options traders. In comparison, the crypto options market is nascent, but growing rapidly. The TVL on DeFi options protocols is only ~$1 billion, constituting a miniscule proportion of the total ~$200 billion locked in DeFi. However, this dynamic is changing quickly; according to Messari, options protocols grew their TVL by 86% in December 2021, even as the TVL in the entire DeFi space actually decreased by 1.5%. And when compared to the value of the options market in TradFi, there is a lot of room for crypto options protocols to grow.

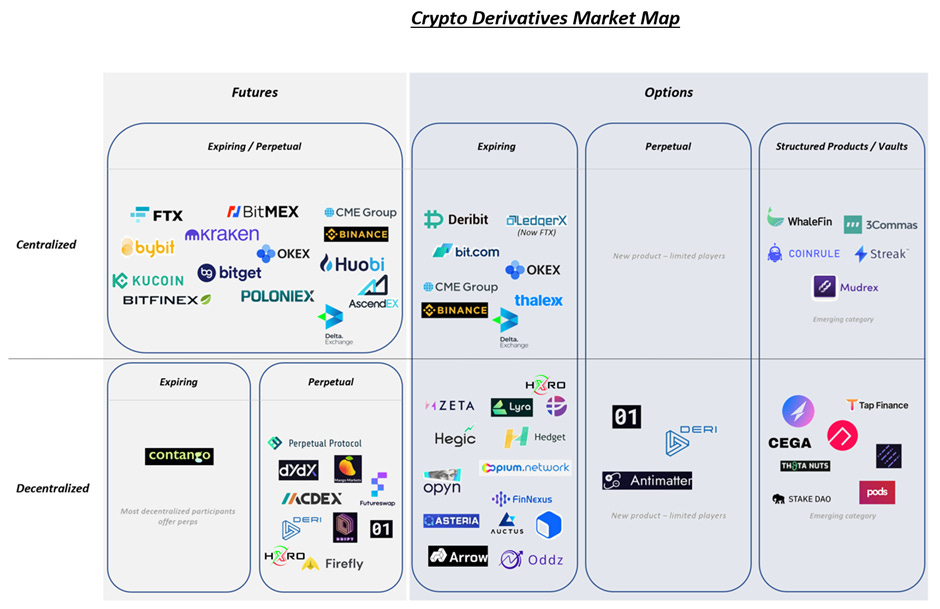

In order to contextualise the crypto options landscape today, Jump Capital’s market map may be useful:

Dopex, a decentralised options protocol built on Arbitrum, occupies the bottom right corner of this map, offering users Single Staking Options Vaults (SSOVs), option pools, and interest rate options. Dopex could be the unlock the crypto options space needs to grow rapidly, with its structured products providing a clean UI and UX and acting as a means to onboard millions of users into crypto. As an on-chain options protocol, Dopex has the advantage of greater efficiency, giving it the ability to charge users much lower fees than centralised exchanges. Dopex’s products are also very easy to use and simple for users to grasp. The mixture of low fees, a clean UI/UX, and easy-to-use products may prove to be a heady combination and a powerful tool for onboarding users.

Dopex’s product set includes:

Single Staking Options Vaults: Users lock up tokens (ETH, BTC, AVAX, BNB, gOHM, etc.) in a vault for a specified time period (day, week, month, quarter, or year) and earn passive yield on their staked assets. The vault then sells call options on these assets to earn premiums and deposits the funds in single-staking DeFi pools to earn additional yield. For stakers, the UX is extremely simple – all they have to do is select the strike prices for the assets they are depositing and let the premiums roll in. The call options are European (meaning that the buyer can exercise them only on the expiry date), although Dopex has recently introduced Atlantic options, which have fixed expiries but the collateral within the options is movable and mobile and can be withdrawn at any time when swapped with the underlying token. The SSOVs offer options buyers a lot of flexibility, with users being able to swap their options for a different expiry or strike price. Users can also trade their vault positions, since every deposit generates a unique ERC-721 token that can be traded on a secondary market.

Option Pools: Users deposit base or quote assets into pools which are utilised as liquidity for purchasers of call and put options. At the end of every weekly or monthly epoch, the users collect their share of pool holdings, any premiums their share has earned, plus DPX token rewards (initially) as an incentive for providing liquidity. Dopex incentivises options buyers by creating volume pools which allow users to deposit funds prior to weekly epochs and use funds from the pool to purchase options from any option pool at a 5% discount.

Interest Rate Options: Dopex could play a critical role in the Curve Wars through the interest rate options product it is planning to offer, where users can bet on the direction of the interest rate of a chosen Curve pool. Convex and [REDACTED] Cartel could use these options to hedge their treasury portfolios or make bets on the interest rate volatility of different Curve pools, and then use their CRV voting power to make their bets pay off. This could drive significant interest to Dopex.

The Dopex ecosystem has two tokens: DPX, the governance token, and rDPX. The supply of DPX is capped at 500,000 and is used to vote on protocol and app level proposals. Value accrues to DPX from fees and revenues from the options pools, vaults, and wrappers built on top of the Dopex protocol. rDPX, on the other hand, has unlimited supply and can be seen as a ‘rebate token’, which is minted and distributed to pool and vault participants who suffer any losses at a rate of 30% of losses that the pool incurs. rDPX can also be used to mint synthetic derivatives that track stocks, commodities, and crypto. The derivatives are minted by depositing an over-collateralised amount of rDPX; for example, $250 worth of rDPX must be deposited to create $100 of synthetic derivatives. If demand for the derivatives grows, more rDPX is locked up, and, in a flywheel, driving up the price of rDPX, which increases the volume of derivatives that can be minted.

Dopex recently overhauled the tokenomics of rDPX, turning it into a deflationary token that will be primarily backed by stablecoins. Dopex plans to create a stablecoin called dpxUSD which can be minted via bonding with rDPX liquidity providers (LPs). While the flow to mint and redeem dpxUSD is complicated and too long for the purposes of this article, you can read more about it here. In a nutshell, each dpxUSD is backed 75% by stable assets and 25% by rDPX. The Average Joe’s Crypto has another great analysis of rDPX v2, where they use Tetranode’s (a crypto whale on Twitter) declaration to vote using his 15M veCRV to bolster dpxUSD’s liquidity in Curve Pools as a proxy to estimate the supply of dpxUSD and the subsequent value of rDPX. The supply of dpxUSD is estimated at a range of values from ~$211m to ~$881m with a middle estimate of ~$350m, while the market cap of rDPX is estimated to have a baseline value of ~$222 million, a ~116% increase compared to today’s market cap of ~$103 million.

The largest risk the protocol faces is the success of dpxUSD – the worst-case scenario would be the stablecoin getting tightly integrated with the rest of Dopex and then failing, which could be a fatal blow. Another risk is that the synthetic derivatives don’t gain traction, which would limit the amount of rDPX locked up and, given its infinite supply, dampen its price over the longer term. All in all, however, given that Dopex is supported by influential whales like Tetranode and DeFi God who intimately understand the crypto space and given the track record of its team till date, it stands a good chance of success.

Alkimiya ⚗️

The most important commodity in crypto is blockspace – the space in a block that includes a transaction. Blockspace is scarce, as there is only a limited amount of space per block. Each transaction that gets submitted to a blockchain is propagated in each node’s mempool, which can be thought of as a list of all transactions waiting to be included in a block. Miners or stakers select which transaction to include next in the block and submitters incentivise them by including a fee with their transactions. The higher the network congestion is, the higher the fee is. Miners and stakers also obtain block rewards for successfully validating a block, which are akin to a stream of cash flows. The problem with fees and rewards, however, is that they can tend to be volatile along with the rest of the crypto market, depending on how network usage fluctuates.

Alkimiya attempts to solve for this volatility by creating a protocol that enables miners to sell their hashpower (the power used by computers to solve hashing algorithms and validate transactions) via bilateral contracts, and by employing a structured products engine that enables users to restructure the contracts into other yield-generating assets (fixed-income bonds, perpetual swaps, etc.) backed by the cash flow of the rewards. The protocol works in a pretty straightforward manner. Miners interact with it via a mining pool they are mining with and Alkimiya only redirects the reward address instead of the physical hashpower. Temporary tokens called Silica represent the ownership of the contracts that will be burnt upon default or redemption and the tokens can be fractionalised and traded on secondary markets. The validation is benchmarked against an index which is used to verify that a validator is delivering its share of rewards.

Alkimiya’s structure enables miners to hedge their risk from the variability of block rewards and fees, obtain upfront payments for their rewards over a period of time by selling hashpower as swaps, or sell calls on the hashpower to boost the yield on their rewards. As the cash flow is represented in Silica tokens, the structured product engine is very flexible and can create any sort of cash flow generating asset, giving users the ability to be maximally capital efficient. Moreover, while Alkimiya is initially incorporating mining rewards, it is looking to add in staking derivatives as well. The primary use cases for Alkimiya include:

Networks that require high levels of computation at the base layer, like Arweave, Filecoin, and Solana;

Any zero-knowledge network that uses GPUs to speed up proof computations;

Hash Vaults (essentially structured products like those of Dopex) that pool together multiple bilateral contracts from multiple Silica owners and restructure the payout into yield-generating assets like fixed-income bonds;

Fee stabilisation for exchanges like Coinbase, which can buy swaps equivalent to the blockspace they use on average and gain the ability to quote fixed fees to users rather than the variable network and platform fees they charge now. This would be hugely beneficial for CEXs and DEXs to hedge against gas fees and would allow them to offer a stable UX to their customers, greatly aiding in their adoption by a larger share of retail users.

The biggest risk for Alkimiya is execution. The product currently isn’t the easiest or most intuitive to use, there are only two listed contracts on the Hashpower Bazaar, and the team hasn’t delivered anything concrete yet, which is understandable since it only launched on Avalanche mainnet a little more than a month ago. While the team has showcased impressive research into the dynamics of blockspace and hashpower, it remains to be seen whether they will be able to deliver on their vision. However, the idea itself is extremely innovative and unlocks a variety of critical use cases built around blockspace, the scarce commodity that will continue to remain at the centre of the blockchain ecosystem.

Closing Thoughts ⌛

Even though the focus on DeFi has waned significantly over the last year and the market’s attention has shifted to other Web3 verticals, this DeFi bear market has led to the survival of the fittest. Innovation has been bubbling along under the hood, with new designs of algorithmic stablecoins and options protocols and the creation of new ‘consensus capital markets’ all leading to products that will potentially form the pillars of the next wave of interest in DeFi as it recovers from being in the Trough of Disillusionment and trudges up the Slope of Enlightenment. I’m optimistic that as these protocols develop over the longer term, they will come to play key roles in maturing the entire Web3 ecosystem.

🔝Reads

Onboarding in DAOs: A Three Sieve Method for More Transparent Onboarding

Inside Starling Lab, a Moonshot Project to Preserve the World’s Most Important Information

To join this journey into the worlds of tech, business, and Web3, subscribe below!

Disclaimer

This is a personal blog. Any views or opinions represented in this blog are personal and belong solely to the article authors and do not represent those of people, institutions or organizations that those authors may or may not be associated with in professional or personal capacity, unless explicitly stated. All content provided on this blog is for informational purposes only. The owner of this blog makes no representations as to the accuracy or completeness of any information on this site or found by following any link on this site. The owner will not be liable for any errors or omissions in this information nor for the availability of this information. The owner will not be liable for any losses, injuries, or damages from the display or use of this information. Any views or opinions are not intended to malign any religion, ethnic group, club, organization, company, or individual.

👇🏽 please hit the ♥️ button below if you enjoyed this post.